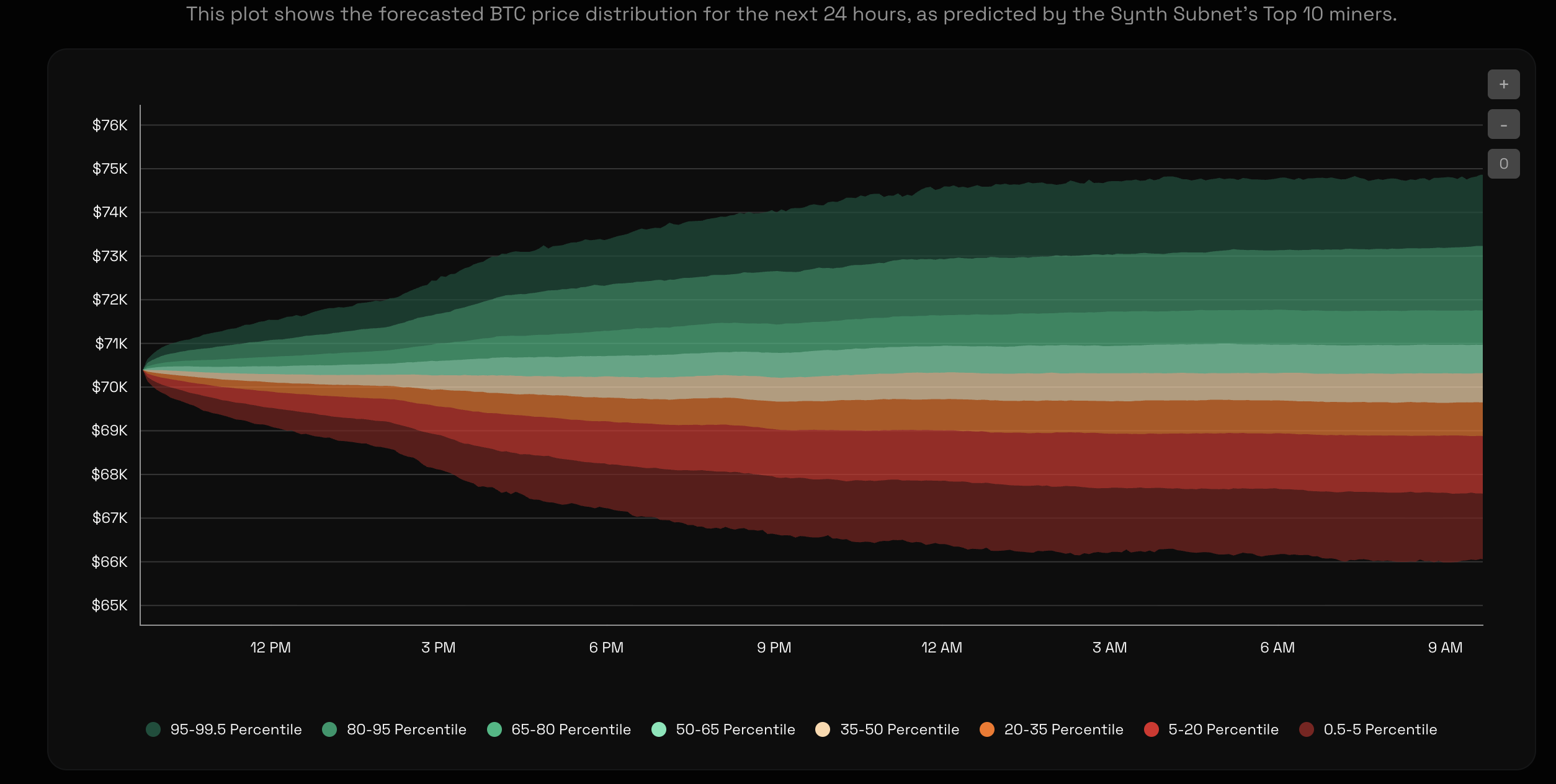

Synth generates forward volatility forecasts for crypto, equities, and commodities - a foundational data layer powering risk models, pricing engines, and automated trading systems

Risk managers and quantitative systems across asset classes rely on realised volatility, historical distributions, and lagging indicators. Very few have access to a continuously updated forward volatility forecast that reflects how price is likely to behave, not just how it has behaved. Most risk models are built on backward-looking inputs rather than a live probabilistic view of future price dispersion

Risk managers and quantitative systems across asset classes rely on realised volatility, historical distributions, and lagging indicators. Very few have access to a continuously updated forward volatility forecast that reflects how price is likely to behave, not just how it has behaved. Most risk models are built on backward-looking inputs rather than a live probabilistic view of future price dispersion

What is forward volatility forecasting and why does it matter?

How is volatility forecasting different from implied volatility?

Which assets does Synth provide volatility forecasts for?

How can volatility forecasts be used in automated trading systems?